7 Statics that Shows Why You Need to Study Financial Literacy

Last year became crucial in the sphere of personal finances. Those who barely stayed afloat have completely run bankrupt. Meanwhile, people who quickly oriented in difficult situations improved their position and survived the crisis.

In such a period, money management is an essential measure. No collateral loans made it easy to get quick financial support. But don’t get carried away with effortless solutions – one day you’ll have to pay for them. True prosperity and stability in finances hide in budgeting skills and understanding of financial processes.

Learn these ways to improve your money management skills to stop living from paycheck to paycheck.

7 Statics that Shows Why You Need to Study Financial Literacy

#1 Save Money for Emergency

COVID pandemic showed us how important it is to save some cash. Everyone can lose a job, need to pay a medical bill, or repair the car. The best variant is to keep a sum, enough for living 3-9 months without any salary. If that’s impossible, at least provide yourself with $1000-5000. Also quite common are situations where Americans are looking for the best emergency loans for bad credit. Such situations are usually caused by pandemics, financial problems in the family and business problems.

Statistics. 38% of American employees don’t have even 1000$ for an emergency. Nothing to say, sum to survive a critical situation should be much bigger. Don’t wait until it’s too late and take measures to protect yourself.

#2 Take Personal Loans Wisely

Unable to take loans in traditional banks, we often turn to personal loans from private lenders. These services are available online and offer soft demands to the borrower – it seems a perfect variant for money support.

The problem is, such accessibility makes some customers irresponsible. As a result, they miss deadlines, don’t collect enough cash for repayment, or forget about small debts. Such attitude leads to the cycle of debts when the clients take more and more money to repay previous debts. Also quite common are situations where Americans are looking for loans for unemployed mothers.

Statistics. In 2020, Bankrate surveyed personal loan customers. They asked people about the reasons for borrowing. Unexpectedly, 38% of them took money to consolidate previous credits.

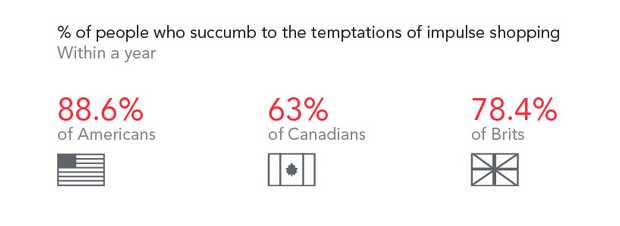

#3 Control Impulsive Buying

Stresses and routine make us spend more – it is a simple way to enjoy yourself in difficult times. Impulsive buying includes food, clothes, unnecessary home items, entertainment, and other stuff you don’t really need.

It doesn’t mean you should avoid all joys and buy only necessary items. Still, think critically before any purchase – ask yourself, whether you really need it or it’s another caprice.

Statistics. Numbers show, Americans spend 5400$ a year on impulsive expenses. Not impressive enough? What about 324 000$ during your lifetime?

To overcome this habit, use a simple exercise: put aside a small sum of money each time you want to buy something useless. Look at the results at the end of the month, and you’ll be surprised with the capital you collected. Would you still like to waste all this cash instead?

#4 Don’t Hesitate and Study Money Literacy

Budget management is a stressful process, which reminds us of all expenses and emergencies, and makes us doubt our salary and achievement. However, you are to learn at least the basics of financial management and introduce them to life.

Now, there are plenty of sources for this goal:

- Blogs and YouTube channels

- Newspapers and magazines, most of which are available online

- Personal finance courses and tutors

- Hiring personal coach

Statistics. 52% of Americans consider financial issues the main source of stress in their lives. Such an attitude makes it even more bounded to organize cash flows and realize opportunities. To stop panicking about your life, educate yourself and take control of your budget.

#5 Start Planning Your Future Today

Time passes quicker than you think. Financial planning is essential for stability and confidence in the coming years. Start with the coming years – plan large purchases, expenses on trips, and entertainment. Such things are easier to collect on.

However, there are more important aspects to think about. No matter what age you are, begin collecting capital for your retirement. You can just collect a needed sum each month, or participate in special saving programs. Deposits in banks are also an easy way to increase your funds.

Statistics. The young generation doesn’t worry about their future. Two-thirds of millennials have no savings for retirement. Other collect small sums, which won’t be enough for a decent living.

It may seem unimportant, but the only way to spend retirement comfortably is to create decent conditions now.

#6 Work on Your Credit Score

Each of your debts and financial operations is recorded in the credit history. Based on that, you get a grade – so-called a credit score. This number determines, whether you can borrow and what conditions are available for you.

If you plan to borrow money or use cards, start with improving this grade. For this:

- analyze your credit history;

- find debts you can repay at the moment;

- check are there any mistakes;

- establish a strategy to repay other issues;

Statistics. Good news – more and more people realize the importance of good rates. FICO claims, the average credit score in the US is rising year to year and was 711 in 2020. It’s a great number, which opens opportunities to borrow at the best possible conditions.

#7 Don’t Underestimate Your Card

Credit cards seem a quick way to take a bit of cash, and quickly return it with no consequences. However, we often lose control over this tool and use it irresponsibly. The only reason to use it is convenience – for example if you forgot the cash at home, or your salary hasn’t arrived yet. In other cases, card debt is as serious as any other.

Statistics. On average, Americans have $5551 debt on their credit cards. Already a decent sum, but add to this the interest – nearly 15-30% depending on conditions. This small may turn to a snowball and surprise you with numbers.

Money management is what makes people sure of their future. If you’re tired of making the ends meet, and panicking about financial issues, start introducing these steps to your daily routine.